The Best Holiday Presents Keep on Giving

It is the holiday season, and I hope your celebration is replete with the joy of giving and receiving gifts to and from friends and family. Now, I’m big on giving gifts that keep on giving, meaning that I like giving and receiving gifts of knowledge.

This year, I have a few holiday presents that you can give yourself and your loved ones that you may not have thought about, but are sure to serve you well in the year ahead.

The gifts I’m talking about today are the gifts of financial preparedness in 2017.

The way I see it, there are several presents you can give yourself right now that can help you become financially prepared for the year ahead. These presents are the best kind because they A) don’t cost you any money, and B) they each represent tools in your investment arsenal that you can use for years and years.

Here are three great holiday presents you can give yourself right now.

1) Cultivate a positive and winning attitude.

By far the biggest present you can give yourself, your friends and your family this year is to approach all aspects of your life with a positive attitude.

While this may sound simple, it’s far from easy, especially when it comes to your approach to investing. What you must remember is that there will be ups and downs in markets, bullish periods and bearish periods for stocks and bullish and bearish periods for different market sectors and various asset classes.

Yet, thanks to the tremendous growth of exchange-traded funds (ETFs) over the past several years, it’s easy to get invested in the segments and asset classes that are outpacing their peers. Having a positive and winning attitude means you are willing to accept the opportunities the market gives you, and that you are willing to embrace those opportunities via targeted ETFs.

In 2017, that’s what subscribers to the Successful ETF Investing newsletter will be doing. So, if you want to see how we go about employing a positive and winning attitude in this service, I invite you to get on board today.

2) Conduct an asset inventory roundup.

The second present you can give yourself this holiday season is to do a little financial summary of all your assets, accounts and financial relationships. This means knowing what assets you own (real estate, stocks, bonds, annuities, mutual funds, 401(k), IRAs, pension plans, etc.), and especially where those assets are held.

This may sound like basic information, but you would be very surprised at how many people I speak with who aren’t sure about where their money is, how it is invested and especially how it should be invested to meet their needs.

This present to yourself requires a little bit of time, but I guarantee that will be time well spent — as knowing where your money is and where it is invested are the first necessary steps toward allowing yourself the third holiday present on your Christmas list.

3) Make your life easier by consolidating your accounts.

Your asset inventory roundup will let you know how many different accounts you have, and in how many different financial institutions your money is located. Once you do this, you’ll need to start giving yourself the present of making your life easier by consolidating your assets into one or two financial relationships.

This means rolling over any former-employer 401(k) accounts into IRAs, or getting out of an old mutual fund company in favor of a discount broker such as Fidelity or Schwab. There is just no good reason to have four, five or more different account statements, or several different brokers, or multiple IRAs or multiple mutual funds at a variety of companies.

Consolidating your investment accounts into one, or at most two, companies will simplify your life immensely, and it also will allow you to make smart changes to your holdings that will enhance your chances of success in 2017.

So, do yourself a favor this Christmas and start giving yourself these three holiday presents. Doing so will be like having Santa coming in for a visit on a regular basis.

If you’d like to find out how you take advantage of the optimism reigning supreme, check out Successful ETF Investing right now!

ETF Talk: Benefit from India’s Fast-Growing Economy

After covering single-country exchange-traded funds (ETFs) for the last few weeks, we are going to move into covering a series of sector-specific emerging market ETFs, beginning with the Columbia India Consumer ETF (INCO).

Sector-specific ETFs seek holdings where companies share a related product or service. As the name of the fund suggests, INCO fully concentrates on investments in the consumer industry in India.

Since its inception in August 2011 under the brand EGShares — a brand that has nine ETFs that all trade within the United States — INCO’s policy has been to hold a maximum of 30 Indian market-cap-weighted consumer stocks. Each of the 30 securities is capped at a maximum weight of 7% of the total portfolio, which helps to provide diversification and more balanced exposure to the Indian consumer sector.

One of the biggest risks investors may face when considering INCO is the fund’s low total assets under management of only $77.81 million. This subjects the fund to liquidity risk and results in relatively high management fees, as is evident in its expense ratio of 0.89%.

However, this does not take away from INCO’s potential. A study by the World Bank has shown that consumption in India is predicted to double from 2015 to 2025. So far, the prediction has held up quite well, with India clocking in as the fourth-fastest-growing economy in the world in 2016 and annual gross domestic product (GDP) growth of 7.5%, according to the World Economic Forum.

To put this in perspective, U.S. GDP has grown by 1.8% this year and China, another emerging markets leader, has grown by 6.7%. INCO provides exposure to Indian companies in the field of automobiles, food, beverages, media and other household products, which all stand to gain from increased consumption brought on by a fast-growing economy.

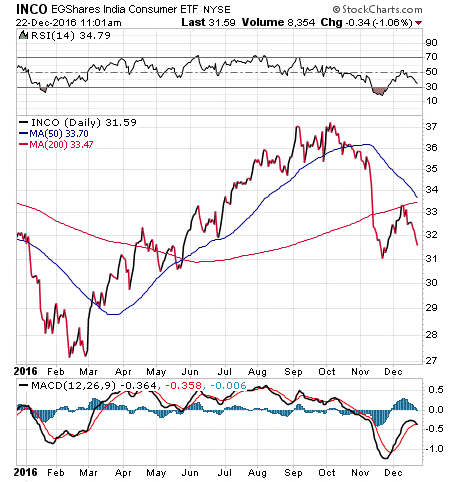

As you can see from the chart below, INCO maintained steady growth from February 2016 through November 2016, when uncertainty on foreign relations rose after Trump’s election as president. It remains to be seen where the fund will head once Trump takes office. INCO’s year-to-date return is 1.12% versus the S&P 500’s 10.82% (as a result of the Trump rally). The fund does not pay dividends.

The fund’s top five holdings are Maruti Suzuki India Ltd, 6.30%; Tata Motors Ltd, 5.91%; Nestle India Ltd, 5.04%; Godrej Consumer Products Ltd, 4.97%; and Bajaj Auto Ltd, 4.96%.

Notice that several of INCO’s top holdings are automobile-related. This is because automobiles are considered to be consumer discretionary products, meaning people will more likely spend money on them as their standard of living increases. If India’s consumption continues to rise as forecasted, automobile manufacturers and distributors could very well be leaders in the Indian economic surge. To take advantage of India’s projected growth, I encourage you to look at Columbia India Consumer ETF (INCO) as a potential addition to your portfolio.

As always, I am happy to answer any of your questions about ETFs, so do not hesitate to send me an email. You just may see your question answered in a future ETF Talk.

Your Year-End Financial Checklist

Only one more week is left in 2016, and that means now really is the time to think about what to do with your investments, and your current financial disposition.

But where do you start?

To answer that, I’ve put together a short list of action steps to take that can get you on the right track to tidying up your current issues in 2016, so that you can be ready to hit the ground running at full sprint in 2017.

1) Review your asset allocation. Do you know what percentage of your money is in stocks, bonds, cash and cash alternatives such as gold or silver? The first step toward knowing where you want to go is to know where you are now.

2) Tax-loss harvesting. If you have some losing, dead-money stocks or ETFs in your portfolio, then now is the time to consider a little tax-loss selling in your taxable accounts. Doing so can take the edge off a big tax bill come April 15.

3) Take advantage of a Roth IRA conversion. A Roth IRA is a great way to keep more of what you have after you retire, and converting a traditional IRA into a Roth IRA might be the easiest way to do that — if your personal situation is right.

4) Give to those you love. Did you know you could give the gift of Roth IRA’s to your adult children and grandchildren? Have you set up a 529 education savings plan for your kids or grandkids yet? How about giving to the charity of your choice? Each of these ways can reduce your overall tax burden, and now is the time to give before the calendar turns.

5) Plan your income streams in 2017. Where will you get your income from in 2017? Will it be from your job, a business, dividend income, annuities, real estate, etc.? Now is the time to make sure you are clear on how much revenue you’ll have coming in next year. Knowing that will help you plan on how much you can afford to spend, and what you can afford to save.

Grinch Wisdom

“Maybe Christmas, the Grinch thought, doesn’t come from a store.”

— Dr. Seuss

Only one more day before Christmas, and I hope you’ve done all your shopping. Yet, amid the hustle and bustle of the holiday, it’s easy to forget that the biggest and best Christmas gifts aren’t material, but rather, “spiritual.” Regardless of your religious beliefs, the holidays are a time to celebrate life, family, good fortune… and the bringing of holiday cheer to the people you care about most. This year, I hope you will celebrate Christmas, Hanukah, Kwanza, or even the winter solstice, by spreading love and happiness all around.

Wisdom about money, investing and life can be found anywhere. If you have a good quote you’d like me to share with your fellow readers, send it to me, along with any comments, questions and suggestions you have about my audio podcast, newsletters, seminars or anything else. Click here to ask Doug.

In case you missed it, I encourage you to read my e-letter article from last week about the effects of the Fed rate hike on financial markets.

Jim Woods is a 30-plus-year veteran of the markets with varied experience as a broker, hedge fund trader, financial writer, author and newsletter editor.

His books include co-authoring, “Billion Dollar Green: Profit from the Eco Revolution,” and “The Wealth Shield: How to Invest and Protect Your Money from Another Stock Market Crash, Financial Crisis or Global Economic Collapse.” He’s also ghostwritten many books and articles, as well as edited content for some of the investment industry’s biggest luminaries. Read more about Jim Woods.