In the Name of the Best Within Us

“Jim, I love your closing salutation on all of your newsletters. The one that says, ‘In the name of the best within us.’ But I was curious, where did you get that and/or how did you come up with that? Thanks in advance, Steven T., Paso Robles, Calif., a loyal reader.”

First off, thank you, Steven, for your question, for the loyal readership and also for knowing the virtue of living in one of the most beautiful and picturesque areas of California, especially if you are a wine nut like me. And I also expect to see you in September at the Whale Rock Music Festival (I go every year, and this year’s just-announced lineup is outstanding).

Now, to your question, “In the name of the best within us” is the title of Chapter X, Part III of what I consider to be the greatest novel ever written, Atlas Shrugged by Ayn Rand.

The novel is an epic tale of adventure, marvelously wide in scope and yet intimately profound. Indeed, it’s no wonder that the novel is cited by so many as one of the most influential books of their lives, and one of the most important novels ever written.

Case in point is my Eagle Financial Publications colleague George Gilder, who called Atlas Shrugged, “the most important novel of ideas since War and Peace.” Writing in The Washington Post in 1986, Gilder explained, “Rand flung her gigantic books into the teeth of an intelligentsia still intoxicated by state power, during an era when even Dwight Eisenhower maintained tax rates of 90 percent and confessed his inability to answer Nikita Khrushchev’s assertion that capitalism was immoral because it was based on greed.”

Now you know one of the many reasons why I consider it an honor to share publishers with George Gilder.

The theme of Atlas Shrugged is the role of man’s reasoning mind in achieving all the values of his existence. Its complex and intricately woven plot is driven by a central and seemingly contradictory question. That question, explains Ayn Rand Institute scholar Onkar Ghate, can be summed up as the following:

“If the men of the mind are the creators and sustainers of man’s life, why do they continually lose their battles and witness their achievements siphoned off and destroyed by men who have abandoned their minds? The story focuses on how the men of the mind learn to ask and to answer this question, thereby putting a stop to their own exploitation.”

Now, a complete analysis of Atlas Shrugged is way beyond the scope of this column; however, I assure you that over the course her magnum opus, Rand demonstrates what happens when those who move the world decide they’ve had enough of being the victims of a society with warped ideas designed to demonize their effort.

I strongly encourage you to read what I consider to be the greatest work of fiction ever written. And yes, I know that at 1,192 pages the novel is a beast to commit to; however, it’s a beast that could quite possibly alter your life in profound ways. I know that it did for me. And as an aside, I found that listening to the audiobook of Atlas Shrugged, as read by the great Scott Brick, was an amazing and immersive experience that was nearly as profound, and dare I say even more dramatic than my first read of the novel in the summer of 1984.

Now, back to the use of “In the name of the best within us,” as my complimentary close. The reason I use that is because of what it means to me, and what it signifies in the novel. I consider it a motto in life, one that I strive to live by in literally every moment.

You see, in any given moment, or in any given decision, or in any moment when we can make a conscious decision, we have the ability to put our best effort into that moment. Indeed, we have the ability to (or not to) give that moment the very best within us.

Put more colloquially, we can choose to do our best, or we can choose to make a modest and half-hearted effort. When we choose to do things in the name of the best within us, that means we choose our best selves.

In the novel, as Ghate writes, “The only reason man has ascended from cave and foot to skyscrapers and locomotives is that there have been individuals like Dagny [one of the novel’s protagonists], who knew what the best within them was and who never let it go — and now these individuals know the meaning and the glory of that which they had been dedicated to.”

Perhaps a passage from the novel’s chief protagonist, John Galt, will provide you with the deeply emotional answer to the question of why I chose, “In the name of the best within us,” as my closing salutation:

“In the name of the best within you, do not sacrifice this world to those who are its worst. In the name of the values that keep you alive, do not let your vision of man be distorted by the ugly, the cowardly, the mindless in those who have never achieved his title. Do not lose your knowledge that man’s proper estate is an upright posture, an intransigent mind and a step that travels unlimited roads. Do not let your fire go out, spark by irreplaceable spark, in the hopeless swamps of the approximate, the not-quite, the not-yet, the not-at-all. Do not let the hero in your soul perish, in lonely frustration for the life you deserved, but have never been able to reach. Check your road and the nature of your battle. The world you desired can be won, it exists, it is real, it is possible, it’s yours.”

***************************************************************

ETF Talk: One ‘CHIQ’ Worth Investing In

Any red-blooded American male will admit — it’s hard not to get caught up in the power of a persuasive “chick.”

But luckily for The Deep Woods readers, this is a special kind of “chick,” and a worldly one, if I may. But, before I go any further, I shall give you some background. This discussion starts in China and potentially ends in your portfolio. Here’s the deal: China has been so battered for so long, that there is a lot of deep value here for the “blood in the ‘red’ streets” investors.

While China battles less-than-favorable headlines, a struggling economic rebound and just an onslaught of difficulties, one area it seems to be excelling in is the consumer. One reason for this may be China’s recently instituted stimulus measures to jumpstart the economy.

Such measures include allowing the People’s Bank of China (PBOC) to hold reduced cash reserves and encouraging banks to lend to qualified developers. Actions such as these have spurred the International Monetary Fund to upgrade its global growth forecast for 2024 by 0.2 percentage points to 3.1%, according to CNBC.

As mentioned, the consumer is the emerging bellwether in China’s resurgence — but keep in mind, it’s important for investors to keep an eye on which specific sub-sectors are participating in this recovery and which are not.

But, valued reader, I would not be keeping true to the “In the name of the best within us,” if I did not share which of the sectors are important to keep an eye on. As it looks, the days of tremendous growth in traditional retail consumption appear to be stalling, but the service sector looks to be leading the charge with Chinese consumers once again pining for travel, making reservations for bars and restaurants and taking to the great outdoors.

Not only are the above categories trending higher, but automobile purchases are poised for growth as well — thanks in part to China’s announcement in 2023 that its main economic planning body created stimuli for increased household vehicle purchases.

Finally, while shock and awe can be fun, it will come as a surprise to no one that China represents the largest e-commerce market globally and continues to maintain that status. In 2023, the retail e-commerce sector saw sales of $3,331 trillion and 2024 forecasts predict upward of $3,565 trillion in sales.

I now will introduce our mystery “chick.”

The Global X MSCI China Consumer Discretionary (CHIQ) is an exchange-traded fund (ETF) that invests in mid- to large-cap consumer discretionary stocks that comprise the MSI China Index. The ETF includes all the major share classes: A-shares and H-shares, red chips, P chips and foreign listings. Now, out of these, the A-shares and H-shares may be the most noteworthy to break down.

H-shares are those traded on Hong Kong’s exchanges and regulated by Chinese law. These are traded in Hong Kong dollars and are freely traded by anyone, foreign investors included. On the flip side, A-shares represent publicly listed Chinese companies that trade on Chinese stock exchanges, including the Shenzhen Stock Exchange (SZSE) and Shanghai Stock Exchange (SSE). Unlike H-shares, these stocks trade in Chinese yuan renminbi (CNY) and Chinese law makes it immensely difficult for foreign investors to buy and sell A-shares.

Thus, our “chick’s” appeal continues to grow, as CHIQ holds both share classes, making it easier for investors to potentially secure stocks that may otherwise be difficult or near impossible to hold.

To sweeten the pot, CHIQ has $238 million in assets under management and its portfolio sells at 11x forward earnings, with five-year revenue projected at 19%. Further, the ETF pays a dividend yield of 2.5%, which is higher than the category average.

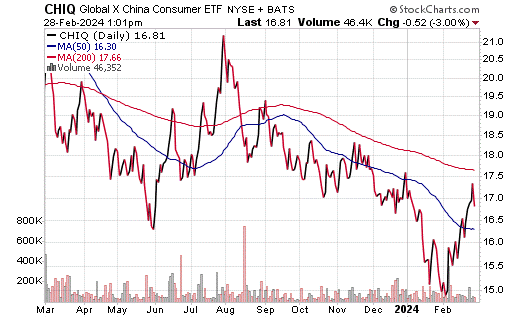

The chart here is a fairly typical depiction of the sector’s fortunes — up and down. However, what this chart also shows is that CHIQ has always able to pull itself from a slump. In fact, for every downward spike, there’s an even higher upward trend, just like the most recent one we are currently seeing.

Courtesy of stockcharts.com

While there was a downward tumble in early February, it has soared almost overnight and is trending back to its normal range within the past month.

Moreover, CHIQ’s portfolio aligns well with the specific areas of consumer spending discussed above, as its first, second and third largest sub-sector allocations are Internet Retail, Motor Vehicles and Apparel/Footwear, respectively. Its top 10 holdings include: PDD Holdings Inc. (PDD), 11.71%; Alibaba Group Holding Limited (9988.HK), 10.21%; Meituan (3690.HK), 6.26%; JD.com, Inc. (9618.HK), 5.56%; 01211 (01211), 4.99%; Trip.com Group Limited (9961.HK), 4.91%; Li Auto Inc. (2015.HK), 3.76%; Yum China Holdings, Inc. (YUMC), 3.52%; New Oriental Education & Technology Group Inc. (9901.HK), 3.37% and ANTA Sports Products Limited (2020.HK), 2.61%.

All quips aside, romance and investing have one thing in common: either is the ficklest of mistresses. But, when it comes to Global X MSCI China Consumer Discretionary (CHIQ), this is one “chick” that potentially ticks quite a few boxes for those interested in overseas portfolio additions.

With an economic jumpstart, the rejuvenation of social and outdoor activities and the country’s growth forecast, it may be time to let China out of the doghouse and make its stimulus work for us — and CHIQ may be just the investment vehicle to do so.

Not only do the holdings align with the specific growing sub-sectors of the Consumer Discretionary world, but it gives investors access to A-shares — which as discussed, are much trickier to obtain and hold outside of China. Moreover, it has a strong five-year growth projection and pays a tidy dividend.

Now that I’ve discussed what this “chick” has to offer, I’d like to rewind a bit and discuss “blood in the ‘red’ streets” investors.

There are several facets to investing, and for many, especially those who lean toward the Way of The Renaissance Man, one of the important ones is history. History is important as it guides us forward, teaches us how not to go backward and lets us soak in the wisdom of those who carved the paths for us.

Baron Rothschild was an 18th-century British nobleman and member of the Rothschild banking family. Rothschild made his legacy fortune buying into the panic that followed the Battle of Waterloo against Napoleon. And, while that is the utterly condensed version, it led to the roughly translated quote: “Buy when there’s blood in the streets, even if the blood is your own.”

Suffice to say, Rothschild was not one to follow the investing pack and was known as a contrarian investor. Simply, the worse things seem in the market, the better the opportunities are for profit.

That, my friends, is what we are doing here. And given the respect I have for readers; I won’t bother further explaining my own “red” tint on the quote — as we all know… China.

I am happy to answer any of your questions about ETFs, so do not hesitate to email me. You may see your question answered in a future ETF Talk.

*****************************************************************

In case you missed it…

NVIDIA and the Super Bowl Champs

What’s the best part about writing The Deep Woods? My answer to this question, which I field frequently, is that I get to make connections between usually disparate fields in order to illustrate something interesting about the world. Today, I am going to do just that once again, this time with the help of my “secret market insider,” i.e. my collaborator in our daily market briefing Eagle Eye Opener.

Now, we all know about the artificial intelligence (AI) enthusiasm that has powered the tech and tech-aligned sectors higher over the past year. Remarkably, the gains in these stocks have accounted for the vast majority of the gains in the S&P 500. But with one-year returns in mega-cap tech stocks at eye-popping levels, a lot of investors are wondering if AI enthusiasm has entered a bubble phase. And with NVIDIA Corp. (NASDAQ: NVDA) set to report earnings after the closing bell today, we wanted to address this issue and investigate if AI tech is in a bubble, and if so, what it means for stocks.

The following is an excerpt from last week’s Eagle Eye Opener, which subscribers received in their inbox at 8 a.m. EST.

First, the impact of AI enthusiasm on the market can be easily demonstrated via any number of startling statistics. NVDA has been the “poster child” of AI enthusiasm because NVDA makes the type of semiconductor chips that power generative AI and demand for those chips has gone through the roof. So, too, has NVDA’s stock, which has gained 218% over the past year. But while NVDA is the proverbial “picks and shovels” of the AI gold rush, other large-cap tech companies such as Microsoft (NASDAQ: MSFT), Meta Platforms (NASDAQ: META), Alphabet (NASDAQ: GOOGL), Amazon.com (NASDAQ: AMZN) and Apple (NASDAQ: AAPL) also have seen large stock rallies as investors expect these companies to harness the power of generative AI to boost revenues and increase earnings and profitability. And it’s not just those stocks. AI enthusiasm has spread beyond tech to “tech-aligned” sectors such as Communication Services (XLC) and Consumer Discretionary (XLY).

Consider these stats:

- More than half of the 23.8% 2023 gain in the S&P 500 was driven by five stocks: NVDA, MSFT, META, AMZN and AAPL. Rallies in those names combined with their weightings accounted for nearly 55% of the gains in the S&P 500.

- Three S&P 500 sectors (Tech, Communication Services and Consumer Discretionary) accounted for nearly 80% of the gains in the S&P 500 in 2023, more fully revealing that last year’s gains in stocks were totally AI-driven.

- At current valuations, NVDA has a market cap worth more than the entire S&P 500 Energy Sector (XLE) and NVDA is worth more, by itself, than the entirety of the Chinese stock market.

- The market cap of the Magnificent Seven stocks combined is larger than every other country stock exchange in the world (second only to the U.S. exchanges).

We can go on and on with these superlatives, but we trust you get the point. So, on to the bigger question: Has the AI mania gone too far and are we looking at a bubble situation?

Based on what most of us think about typical bubbles, the answer is “no,” they are not in a bubble, and here’s why. Their valuations really haven’t changed despite these massive share price increases.

We looked at the forward- and backward-facing price-to-earnings (P/E) ratios of five of the Magnificent Seven stocks (NVDA, MSFT, AAPL, META and AMZN). While there’s been some volatility over the years with Covid and other surprises, by and large, the forward- and backward-looking P/Es of these stocks are roughly where they were over the past several years, including before Covid and before AI mania.

This is an important distinction between now and the late 1990s/early 2000s, when the P/Es of tech stocks exploded higher, revealing unsustainable valuation expectations. The fact that forward or backward P/Es haven’t changed much reveals a very important reality of this AI-stock-driven rally in tech: It has occurred because these companies are making a lot more money, not just because people hope these companies make a lot more money.

We reviewed the actual earnings of the five stocks referenced above (NVDA, MSFT, META, AMZN, AAPL) and the results were remarkably consistent. Across the board, these companies are earning 2X-3X what they were just several years ago, and EPS for all of them are at or near multi-year highs. So, a large part of the rally in these stocks has been driven by actual earnings growth. These companies are making a lot more money, so their shares are worth a lot more!

The conclusion of this research is clear. The AI-driven rally in the “Mag Seven” is largely justified by the fact that they’re making a lot more money than they were previously. As such, their stocks should rally! But that does not mean this historic move higher in the Mag Seven or tech/tech-aligned sectors doesn’t pose a risk to the market. It does.

The easiest way to explain that risk is that the performance of the Mag Seven (from earnings growth and stock appreciation) is essentially making the rest of the market look a lot stronger than it actually is. And if the Mag Seven stocks stop performing like money-printing factories, then the market as a whole is worth a lot less than people think. Here’s a stat that explains what I’m talking about.

In 2024, analysts expect the S&P 500 to earn about $243 per share. Over the next 12 months (so, basically 2024), analysts expect earnings from just the Mag Seven stocks to account for $74 of those $243, or about 30% of 2024 earnings for the S&P 500. Put differently, 1.5% of the S&P 500 is expected to account for 30% of the index’s earnings. If these seven stocks do not deliver, then earnings expectations for the S&P 500 will get revised sharply lower, and that’s where the risk lies.

Here’s a slightly easier way to explain it. The stock market is kind of like the Kansas City Chiefs (for all you football and Taylor Swift fans). The Kansas City Chiefs, like the S&P 500, had an amazing year, winning the Super Bowl. But the team doesn’t have that many great players, except the two especially amazing players. Quarterback Patrick Mahomes and tight-end Travis Kelce are so good that they produce results far above what the rest of the team should expect. Essentially, those two players help produce results for the team that are much better than the team’s aggregate talent level would warrant or imply.

Similarly, the historic AI-driven earnings growth in the Mag Seven is producing returns for the S&P 500 far above what the “rest” of the market would warrant based on actual earnings. And as long as they (Mahomes, Kelce and the Mag Seven) continue to perform, the Chiefs (and the S&P 500) can keep winning. However, if one falls off or gets injured, then the reality that the rest of the team isn’t that good will be exposed, and the Chiefs will likely quickly go from Super Bowl champs to just another team.

Completing the analogy, the Mag Seven stocks are the “MVPs” of the 2023 rally, but their amazing earnings growth and performance is masking an otherwise average rest of the market, and if earnings growth doesn’t meet expectations, then the average nature of the rest of the market will be exposed (and a decline in the S&P 500 will likely follow).

So, what does this mean for markets? From a tactical standpoint, the takeaway from this analysis advocates for allocations to the Invesco S&P 500 Equal Weight ETF (NYSEArca: RSP), unless you are a true believer in the never-ending profit generation of the Mag Seven. I say that because if the Mag Seven disappoints versus expectations and AI isn’t as profitable as expected, we’re going to see their earnings drop while other, unrelated sectors (that have lagged) are unaffected. So, we’ll likely see a reversal of the 2023 market, where the S&P 500 drops on tech while RSP outperforms and closes.

Conversely, if the Mag Seven meet expectations, they’re just fulfilling what’s already expected and as such, we could see investors continue to rotate into other parts of the market to try and capture some relative value, as RSP is trading at a near-20% valuation deficit to SPY. The only scenario where the Mag Seven names continue to lead markets higher is if AI’s ability to maximize profits is greater than expected. And while that may turn out to be true, we do think the expectations for AI are pretty lofty here.

*****************************************************************

Specializing in Everything

“A Renaissance Man is one who specializes in everything.”

–He Who Must Not Be Named

At a gathering of friends recently, someone asked me, “Jim, what is a Renaissance Man?” Before I could reply, an often-obnoxious acquaintance of mine broke into the conversation and said, “A Renaissance Man is one who specializes in everything.” Now, this man, let’s call him “He Who Must Not Be Named” (for all of you Harry Potter fans) thought he was being clever and sarcastic with his remark.

Yet, I flipped the script on him and said, “Yes, that is a great description of the Platonic form of a Renaissance Man.” I knew the Plato reference wouldn’t be lost on him, because He Who Must Not Be Named is a highly educated man. Yet, I went further to explain that the goal of a Renaissance Man is to know enough about many disparate things so that he can become one that specializes in everything. And, as I also explained, while it is literally impossible to specialize in everything, it’s the process of learning these things along the way that is an end in itself.

Wisdom about money, investing and life can be found anywhere. If you have a good quote that you’d like me to share with your fellow readers, send it to me, along with any comments, questions and suggestions you have about my newsletters, seminars or anything else. Click here to ask Jim.

In the name of the best within us,

Jim Woods

Jim Woods is a 30-plus-year veteran of the markets with varied experience as a broker, hedge fund trader, financial writer, author and newsletter editor.

His books include co-authoring, “Billion Dollar Green: Profit from the Eco Revolution,” and “The Wealth Shield: How to Invest and Protect Your Money from Another Stock Market Crash, Financial Crisis or Global Economic Collapse.” He’s also ghostwritten many books and articles, as well as edited content for some of the investment industry’s biggest luminaries. Read more about Jim Woods.