Come On Get Higher for Longer

- Come On Get Higher for Longer

- ETF Talk: Dabbling in Debt with This ETF

- The Actual Meaning of a ‘Midlife Crisis’

- Betting with A French Novelist

***********************************************************

Come On Get Higher for Longer

There’s a fantastic song by the great Matt Nathanson that I’ve always loved called, “Come On Get Higher.” Here’s an acoustic version of the song from a 2013 appearance at Amoeba Records in San Francisco, where coincidentally, your editor happened to be that day. Now, I bring up this song title today because it reminds me of what the market is facing right now, and that is the headwind that is “higher-for-longer” interest rates.

As we wrote this morning in the daily market briefing, Eagle Eye Opener (which you simply must subscribe to, if you want to know what real professionals are watching each trading day), the recent stall in the stock market rally has coincided with a quiet, but important, evolution in the outlook for Federal Reserve monetary policy, as investors have started to focus on what’s “next” from the Fed, namely rate cuts. And over the past two weeks, rate cut expectations have been solidly pushed out, and that’s contributing to the upward pressure on yields and a growing headwind on stocks.

Now, we understand that it might seem somewhat premature for the market to be focused on when the Fed cuts rates, considering we may get another rate hike before year-end. But that’s just testament to the reality that the market is always looking for what’s “next,” and with the Fed done (or almost done) with rate hikes, what’s “next” is rate cuts.

Broadly speaking, investors had previously anticipated a rate cut as early as March 2024. But over the past month, that’s been pushed out to May and that has contributed to the rise in the 10-year yield and the headwind on stocks, because the longer it takes for the Fed to cut rates, the greater the chances of a hard economic landing, and the reason is clear: The longer rates stay high, the more pressure on the economy, and the greater likelihood that an economic contraction occurs.

Going forward, it’s not so much about how high rates go (barring a major surprise of two or more rate hikes), but instead how long they stay high.

That’s also why 2024 year-end fed funds estimates have become important. Right now, markets expect year-end 2024 fed funds to end at 4.33%. That reflects 100 basis points of rate cuts in 2024 (starting in early 2024). Here’s the problem: That is fewer cuts than the market expected a month ago.

One month ago, the market was pricing in a year-end fed funds of around 4.10%, or another 25 basis points of cuts next year. Now, that number has drifted higher thanks to solid economic growth and a lack of a big decline in inflation. So, why does this matter to you?

It matters, because if the market pushes out the timing of the first rate hike (June or beyond) or increases the expectations for year-end 2024 fed funds (meaning there will be fewer cuts next year) then that will act as a hawkish headwind on stocks and boost Treasury yields further (10-year Treasury yield above 5%?) and that, in turn, will increase hard landing chances and weigh on stocks.

Because of this reality, and until the market dynamic changes and this is no longer necessary, our Eagle Eye Opener will include commentary on the data so you know 1) At what point markets expect the first rate cut, and 2) Year-end 2024 fed funds expectations.

That way, we can see whether the market expectation is becoming more hawkish (negative for stocks and bonds), because if the market begins to price in a higher-for-longer interest rate environment, that will be a new and substantial headwind on stocks — and that would require getting more defensive in portfolio allocations.

P.S. Come join me and many of my Eagle colleagues on an incredible cruise. If you book before Sept. 29, you’ll receive a spend-as-you-wish $250 ship board credit! In addition, this is all-inclusive — meals, drinks and even the excursions are included in your one-time price!

We set sail on Dec, 4 for 16 days embarking on a memorable journey that combines fascinating history, vibrant culture and picturesque scenery. Enjoy seminars on the days we are cruising from one destination to another, as well as dinners with members of the Eagle team. Just some of the places we’ll visit are Mexico, Belize, Panama, Ecuador and more! Click here now for all the details.

***************************************************************

ETF Talk: Dabbling in Debt with This ETF

As my readers know by now, I aim to live life to the fullest and sometimes that includes taking risks, which I have relayed in past issues of The Deep Woods, but there is a difference between calculated risk and unnecessary risk.

So, while the economy may be poised for a soft landing, given the recent string of positive economic reports in the United States, stronger-than-expected earnings growth and a surprisingly resilient job market, it doesn’t mean this possibility will come to fruition. With this in mind, I tend to be of the mindset that padding your portfolio with lower-risk ETFs may be a wise decision.

This is where the Franklin Senior Loan ETF (FLBL) comes into play. FLBL is a fund that aims to produce a high level of current income and preserve capital. Produce and preserve – two words that every investor should like.

The fund invests in U.S. dollar-denominated senior loans of both U.S. and non-U.S. companies. However, its exposure to non-U.S. issuers is capped at 25%.

The debt FLBL invests in is mostly floating rate and sub-investment grade, with a rating of B- or better. However, just like yours truly, this fund also takes certain calculated risks and up to 25% of its holdings may have a lower credit rating. Here’s why I am calling this a calculated risk: investing in debt with a lower credit rating can generate higher yields than debt with higher ratings.

FLBL invests in debt with floating rates, which can virtually eliminate the interest rate risk of a portfolio. The downside here is that the credit risk can increase if the issuers are struggling to make larger payments when rates rise.

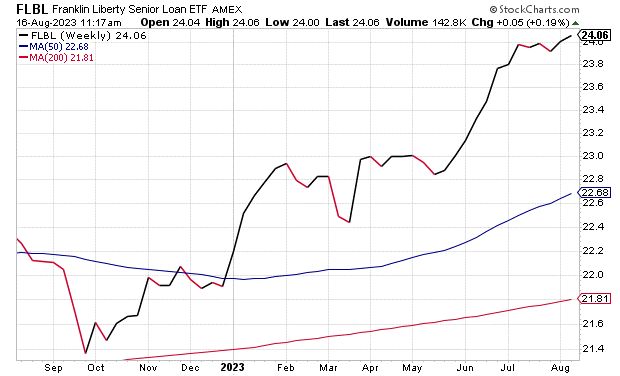

Formed in 2018, FLBL has assets under management of $226.33 million and net assets of $227.54 million. Now, while those numbers are not in the billions of dollars — it has a tantalizing dividend yield of 7.80%. Moreover, when looking at the chart below, FLBL is trading at $24.22, the highest end of its 52-week range. As of this writing, the fund is trading at $24.06. In addition to that, FLBL’s 50- and 200-day moving averages are steadily climbing and have been doing so during the last few months of 2022.

Source: Stockcharts.com

In terms of holdings, Financial Services makes up 71.42% of the fund’s weighting. And 92.53% of its composition is comprised of bonds.

Overall, dabbling in debt sounds far riskier than it may prove to be, as the sole purpose of the fund is to produce and preserve income – and that is what our goal is while we wait to see where the economy goes.

Further, not only does the fund have an incredible dividend yield, but it’s also trading at its peak and is proving its stability through its moving averages. So, for investors who may be intrigued by a little calculated risk, Franklin Senior Loan ETF seems worth considering.

As always, I am happy to answer any of your questions about ETFs, so do not hesitate to send me an email. You may just see your question answered in a future ETF Talk.

*****************************************************************

In case you missed it…

The Actual Meaning of a ‘Midlife Crisis’

I just celebrated another trip around the sun, and based on my year of birth, I am still clinging to the age range where people like to ask you if you’re experiencing a “midlife crisis.” Fortunately, nobody that actually knows me has asked me this because they know better.

You see, usually people’s intention with this comment is pejorative, one aimed at a subtle and passive-aggressive criticism of another for the very real feelings of self-assessment and desire for peak experiences in what’s left of one’s life.

The standard bromide here is that if a man (and it’s almost always a man who’s scolded with this pejorative) wants to experience some actual fun in life, either through buying a motorcycle or a McLaren or entering into an exciting, new loving relationship with someone who sees his value, that he has somehow regressed into a state of lost and willful adolescence.

Well, to anyone out there who criticizes or critiques or otherwise derides another with the comment, “he’s just going through a midlife crisis,” my response is — why are you criticizing another for wanting to experience life to the fullest?

Why is your conception of what a middle-aged man “should” do of any relevance to the way that middle-aged man chooses to live his life?

What I have found to be the case is that those who sling arrows at others for how they choose to live their lives are often those who need that arrow aimed directly at themselves. “Misery loves company” is the adage that comes to mind here, because all too often, the “he’s just going through a midlife crisis” critique comes from a place of latent and/or explicit jealousy over someone choosing to experience life on their own terms.

The philosophic underpinnings that give rise to this sentiment are easy to identify. The ethics so prevalent and so ingrained in the culture for thousands of years are those of self-sacrifice, suffering, duty and the so-called “moral good” of living your life in the service of others. Your life is transient, and doesn’t really matter, so say these ethics. What really matters is your service to others, to the group, to society and to the collective.

Yet, ask yourself this: Why doesn’t your life matter just as much as anyone else’s life?

Isn’t your life the only one you can live? Moreover, don’t you have the right to be happy? Or is your happiness somehow a source of moral turpitude?

According to my ethics, the ethics of rational egoism and rational self-interest, you have the right to your own life, and your own achievement and your own pursuit of your own happiness. You don’t have the right to sacrifice others to your cause, nor do you have the duty to sacrifice your happiness to others.

The chief exponent of this philosophic view is novelist/philosopher Ayn Rand. In her magnum opus, “Atlas Shrugged,” the protagonist, John Galt, puts this theory of ethics in brilliantly succinct and powerful form during the climatic speech scene:

“A morality that dares to tell you to find happiness in the renunciation of your happiness — to value the failure of your values — is an insolent negation of morality. A doctrine that gives you, as an ideal, the role of a sacrificial animal seeking slaughter on the altars of others, is giving you death as your standard. By the grace of reality and the nature of life, man — every man — is an end in himself, he exists for his own sake, and the achievement of his own happiness is his highest moral purpose.”

Indeed, one of Rand’s most-brilliant contributions to intellectual history is this defense of one’s pursuit of one’s own moral happiness and rational self-interest. And because this view challenges thousands of years of conventional morality so deeply ingrained in us all, it’s both difficult and, at first, somewhat uncomfortable to consider.

Yet, when we do stop and really contemplate the idea of rational egoism, we realize that however difficult our struggles may seem, the pursuit of our own happiness is our highest moral purpose, whatever we deem that happiness to be — even if that happiness comes to us in the form of a midlife motorcycle.

*****************************************************************

Betting with A French Novelist

“Often the difference between a successful person and a failure is not one’s better abilities or ideas, but the courage that one has to bet on one’s ideas, to take a calculated risk — and to act.”

— Andre Malraux

If you know me, you know that my family’s heritage (on my father’s side) can be traced back to France. In fact, my last name “Woods” is a translation from the French word “DuBois,” which means “of the woods.” Now, my penchant for French literature (Hugo, Proust, Voltaire, Dumas, Verne) could be related to my heritage, but it also could be because many of these writers had a flare for language, deep ideas, and for living the “Renaissance Man ethos,” including the novelist and statesman Andre Malraux, who provides this week’s quote.

You see, when it comes to success in life, and certainly in investing, courage and the willingness to take action are two of your greatest weapons. Hey, leave it to a fellow Frenchman to sing that point home!

Wisdom about money, investing and life can be found anywhere. If you have a good quote that you’d like me to share with your fellow readers, send it to me, along with any comments, questions and suggestions you have about my newsletters, seminars or anything else. Click here to ask Jim.

In the name of the best within us,

Jim Woods

Jim Woods is a 30-plus-year veteran of the markets with varied experience as a broker, hedge fund trader, financial writer, author and newsletter editor.

His books include co-authoring, “Billion Dollar Green: Profit from the Eco Revolution,” and “The Wealth Shield: How to Invest and Protect Your Money from Another Stock Market Crash, Financial Crisis or Global Economic Collapse.” He’s also ghostwritten many books and articles, as well as edited content for some of the investment industry’s biggest luminaries. Read more about Jim Woods.