Tonight We’re Gonna Party Like It’s 1968

Social unrest, violence in the streets sparked by racial tensions, political tumult, a hotly contested election, a viral plague raging throughout the globe — and a brilliant achievement that put Americans into Earth’s orbit.

No, I’m not talking about our current reality.

Instead, I’m referring to the year of our Lord one thousand nine hundred sixty-eight. Yes, the summer of 1968 is turning out to bear an eerie resemblance to the spring of 2020.

Think about it: more than five decades ago, we had rioting in American cities over the ugly war in Southeast Asia and the assassination of the Rev. Martin Luther King, Jr. We had Nixon vs. Humphrey, we had the H3N2 avian flu that killed over 100,000 people — and we had Apollo 8, the first crewed spacecraft to successfully orbit the Moon and return to Earth.

This year, we have social unrest in the streets sparked by the killing of George Floyd (we also have the ongoing war in Afghanistan, but sadly, Americans have largely forgotten about this tragedy). Then we have a neck-and-neck race between President Trump and former Vice President Joe Biden, a contest that promises to be an all-out political brawl. Of course, we also have the devastating viral cloud that is COVID-19, a much worse global pandemic than any we’ve seen in over a century — and then we have the majestic human achievement that is SpaceX’s voyage to the International Space Station.

As Mark Twain once quipped, “History doesn’t repeat itself, but it often rhymes.” Or, as the more contemporary musical poet, Prince, might have phrased it, “Tonight we’re gonna party like it’s 1968.”

Now, I could spend a lot of time railing about the evils of state brutality, the ugly philosophic root of racism, the destructiveness of the coronavirus lockdowns and the tribalism about to play out over the presidential election. Yet those who know me best won’t be surprised to learn that while I could dissect these bad ideas with a rational rapier that William of Ockham would envy, I prefer to unleash the lance of praise on the space launch.

You see, violence, rational animus, government overreach and viral scourges are all part of the current human condition. Yet the more important part, the noble part, the laudable part, the part that makes me feel proud to exist, is the part expressed to us by Elon Musk and the brilliant men and women who successfully launched the first-ever commercial manned space mission.

Last year, I wrote about the 50-year anniversary of the Apollo 11 mission. The title of the piece was, “This Is What Man Can Do.”

Here, I honored the achievement that culminated on July 20, 1969, when Neil Armstrong became the first man to walk on the moon. That seminal event remains, to this day, an example of the very best within us. Here’s how I phrased it last year:

I was only a five-year-old when that “one small step for man, one giant leap for mankind” took place, yet it was my first real memory of a life event. And, I must say, history couldn’t have picked a better, more heroic, first memory to shape a young man’s psyche.

In that article, I also explained that my philosophic insight into Apollo 11’s true meaning came to me from novelist/philosopher Ayn Rand. I discovered her works in the early 1980s, first via “Atlas Shrugged,” then “The Fountainhead” and then subsequently read every work of hers — fiction, non-fiction, op-eds, essays, lectures, letters, whatever I could get my hands on.

Here’s how Rand thought of this glorious event:

“What we had seen, in naked essentials — but in reality, not in a work of art — was the concretized abstraction of man’s greatness… For once, if only for seven minutes, the worst among those who saw it had to feel — not ‘How small is man by the side of the Grand Canyon!’ — but ‘How great is man and how safe is nature when he conquers it!’

“That we had seen a demonstration of man at his best, no one could doubt… and no one could doubt that we had seen an achievement of man in his capacity as a rational being — an achievement of reason, of logic, of mathematics, of total dedication to the absolutism of reality.”

When I watched the SpaceX Falcon 9 and Dragon launch on Saturday, I felt the pride of being human. No, I didn’t have any direct hand in the launch, aside from recommending Tesla Motors (TSLA) stock many times over the years (it’s been one of my biggest winners). Yet I still felt connected to this achievement as a member of the human race.

So, as our cities burn in protest, as looters usurp property rights, as state governments continue imposing shutdown orders and as we prepare for a contemptible political donnybrook in the fall, remember what man can do when he trains his reason on a noble goal.

Remember that majestic achievement is possible and that the best within us all is achievable — if we choose it.

**************************************************************

ETF Talk: Low Duration Income ETF Offers Protection From Low Rates

(Note: Third in a series on the biggest actively managed ETFs)

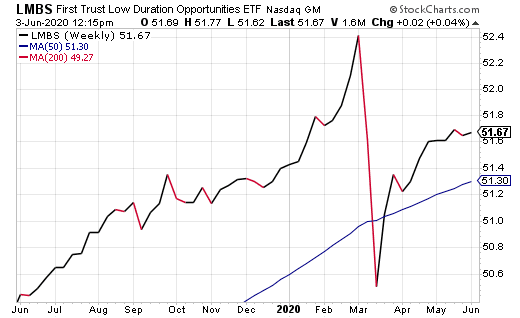

The First Trust Low Duration Opportunities ETF (NASDAQ:LMBS) is an actively managed, fixed-income fund that invests in an array of mortgage-backed securities and has a target duration of less than three years.

LMBS, an open-ended fund, occasionally will take positions in U.S. Treasury future bonds or options. It is among few exchange-traded funds (ETF) of its kind to focus on short-duration mortgage-backed securities.

The ETF invests in federal-agency-backed mortgage securities, as well as those from non-agencies and commercial issuers. By doing so, the fund raises its relative value and yield.

LMBS has a 0.67% expense ratio and a dividend yield of 2.24%. This MBS ETF has $5.26 billion in net assets and a net asset value of $51.67, with $5.39 billion in assets under management. Year to date (YTD), this fund’s total return is 0.64%.

Since December 2019, this fund has managed to climb and currently is above its 50-day moving average. Much like the rest of the market, this fund saw a drop in mid-March, with its lowest close YTD of $49.40 on March 23. However, as the chart below shows, it has started to make a recovery with a strong rise in early April, following a decent jump on March 27, when the closing price reached $51.25.

LMBS seeks to generate current income with a secondary objective of capital appreciation. In normal conditions, the fund seeks to achieve its investment objectives by investing at least 60% of its net assets in mortgage-related investments.

This non-diversified fund’s portfolio composition is 80.91% bonds, 19.08% cash equivalents and 0.01% other. Its top 10 holdings make up 48.56% of its total assets. The top five holdings as of June 2, according to Morningstar, are Federal National Mortgage Association 2.5%, 9.28%; Federal National Mortgage Association 2%, 4.97%; Fnma Pass-Thru 2.5%, 3.04%; Fnma Pass-Thru 4.5%, 2.78%; and Fnma Pass-Thru 2.5%, 2.07%.

This fund’s portfolio carries more of a material risk because it includes non-agency and commercial mortgage-backed securities. However, its short target duration has an increased appeal for investors worried about rising interest rates and still wanting a decent yield. This is a readily tradable ETF and has a solid daily volume.

In sum, while there is more risk in First Trust Low Duration Opportunities ETF (NASDAQ:LMBS), than in purely agency-backed MBS funds, it has made YTD gains and has not faltered much since its 2014 inception. With a low duration of less than three years, it is more protected from rising interest rates than some other ETFs. According to Yahoo Finance, LMBS has a bond rating of 98.15% in the AAA sector, which is a positive given that the majority of its portfolio consists of bonds.

As always, I am happy to answer any of your questions about ETFs, so do not hesitate to send me an email. You just may see your question answered in a future ETF Talk.

********************************************************************

In case you missed it…

Do the Twin ‘Ds’ of Deficits and Debt Still Matter?

One of the most frequently asked questions I receive from investors, whether it is at a conference such as the MoneyShow or FreedomFest, via email from readers or at any social gathering where people know about my occupation, has to do with what are sometimes called “the twin Ds,” i.e. deficits and debt.

This subject has become of particular interest to many, given the massive deficits and debt headed our way due to the government’s multi-trillion-dollar stimulus packages to fight the coronavirus pandemic. But just how massive is that debt?

Well, last week, the U.S. Treasury sold 20-year Treasury bonds for the first time in 34 years in response to the colossal amount of debt that needs to be raised to pay for the various stimulus packages. Not surprisingly, the resurrection of that bond further fueled a debate about whether the exploding debt that is funding the coronavirus response will be a long-term negative for the economy, the dollar and, by default, investors.

Up until this pandemic, the question of deficits and debt wreaking havoc on the economy was more of an academic argument. That’s not the case any longer. Why? Because most adults know that it’s impossible to always spend more than you take in and simply keep adding more and more debt without something really bad happening. And that personal knowledge is being extrapolated out to the U.S. government’s finances as the multi-trillion-dollar stimulus packages rack up.

To help me unpack the question of whether the ramp-up in the twin “Ds” is going to represent a serious threat to the economy and the markets, I turned to my friend and brilliant colleague, macro analyst extraordinaire Tom Essaye of Sevens Report Research.

Tom is a regular contributor to my Successful Investing and Intelligence Report newsletters, and he’s also the editor of a highly recommended daily publication called the Sevens Report.

Here are a few thoughts we bandied around during a recent discussion we had on this hot topic.

Jim Woods (JW): I am constantly being asked about deficits, debt and the buildup of both as they relate to the potential negative consequences they can have on the economy and the markets. These days, those questions are more relevant than they’ve ever been. What’s your assessment of this situation?

Tom Essaye (TM): I think the concerns over the massive new levels of spending and the resulting deficits and debts to follow, are justifiable. Yet while we should be concerned, the deficit and debt are unlikely to derail the U.S. economy or the market over the longer term.

JW: Why do you say that?

TM: The reason comes down to one key factor, and it’s the so-called “TINA” trade, i.e. “There Is No Alternative” to either U.S. Treasuries or the U.S. dollar. Yes, it’s totally true that an already “not good” U.S. fiscal situation has been made exponentially worse by the coronavirus fallout and stimulus packages. Numerically speaking, consider that the U.S. deficit-to-GDP ratio will spike from about 4% in 2019 to nearly 20% in 2020!

Put in real dollar terms, the U.S. federal deficit was about $1 trillion per year at the end of 2019. It is expected to be $3.7 trillion by the end of September, and that’s not including the latest $3 trillion stimulus bill working its way through Congress. Meanwhile, U.S. GDP in 2019 was about $21 trillion. Let’s say it’s down 5% to $20 trillion in 2020. That means that the budget deficit for 2020 will be around 18%. That’s much higher than the 10% peak following the financial crisis. In fact, that’s the highest deficit-to-GDP percentage since World War II!

JW: Given that increase, you would think that global investors would be selling the U.S. dollar and Treasuries. But instead, the opposite is happening.

TE: Yes, and the reason why is because every other country is in a similar situation. In fact, every major economy, including the countries of the European Union, Britain, China and Japan, all are having to raise massive amounts of money to offset the negative impact from the coronavirus. And since currencies and global bonds are all relatively priced, the net effect is that everyone’s fiscal standing has been downgraded, not just the United States’. Given that, there remains no alternative (TINA) to U.S. Treasuries.

Put plainly, the United States is in not good fiscal shape, but so is virtually everyone else, and since capital needs to be placed in assets where investors are confident it will hold value, there remains nothing that can challenge the size and stability of the U.S. Treasury market. It may confound economic fundamentalists, but the simple truth is that demand for U.S. debt is surging despite the explosion in the deficit, and that’s because Treasuries remain the safest, most liquid sovereign bond in the world — despite the exploding deficits and debt.

JW: I suppose that until something (i.e. a sovereign bond) can challenge that, which I don’t see on the horizon, then the global market will tolerate a deteriorating U.S. financial situation far longer than the economic purists might think.

TE: Exactly. And as for the dollar, well, it remains the world’s reserve currency, and that also helps give the U.S. a “pass” on a lot of her fiscal problems. Last week, I read that approximately 50% of the world’s debt is priced in U.S. dollars. That means the world needs a lot of dollars, and that puts the U.S. in a very powerful position. It also incentivizes the global economy to support the value of the dollar and keep it stable, because if it becomes unstable, everyone loses. So, while it’s not fiscally responsible, the U.S. debt and deficits don’t matter to stocks as long as the U.S. is able to sell Treasuries to finance the gaps.

JW: I guess that means that U.S. deficits and debt won’t matter until they become so bad that global investors don’t want to buy Treasuries anymore.

TE: Yes, and that won’t happen until the U.S. fiscal situation gets a lot worse, or there becomes a viable alternative to U.S. Treasuries or the U.S. dollar in the global bond and currency markets. None of those events are looming, and as such, despite the negative headlines, the deficit and debt are unlikely to hurt the equity rally or the economy near term.

Now, just to be clear, I’m not telling you or your readers that deficits and debt will never matter. I think that if left unchecked, and the deficit runs through 30% in the coming decades, then yes, at some point the market will begin to shy away from Treasuries. At that point, financial hell will break loose. And if things don’t change in the trajectory of the U.S. fiscal position, that will happen one day, but it’s very unlikely to be a day anytime soon.

JW: So, while deficits and debt make for interesting conversation, they aren’t going to be an immediate market influence unless there’s a massive and rapid deterioration.

TE: I think that’s right, and I think that while it’s something to have on our radar, for now it’s not a reason to let fear of the twin Ds keep you from investing and growing your money.

JW: Thanks Tom, as always, you’ve been a rational lighthouse in a fog of COVID-19 uncertainty for myself and my readers.

P.S. Did you watch my live summit, “Action Plan for the Wipeout and Recovery”? If so, I hope you found it interesting and actionable. If you missed it, don’t fret. This timely emergency briefing on how to handle this volatile market is too valuable, so we made sure you can watch a replay of the event right here. Don’t miss this special presentation, and don’t miss out on learning about three of my favorite trades designed to double your money!

*********************************************************************

On Working Through It

“I’m done crying. Now I’m just working through it.”

–Kathy “Moon Owl” Quinn, proprietor, Moon Owl Nocturnal Eats

The recent civil unrest and the aggregate infringement on our rights by both government and individuals has had a lot of adverse consequences. That’s especially true for businesses hit by looters, especially businesses such as retail and restaurants that were just beginning to reopen after months of coronavirus lockdown.

Yet as my friend, entrepreneur and chef extraordinaire Kathy Quinn of Moon Owl Nocturnal Eats, bravely remarked, the time is done for crying. Now, you just have to work through it. It’s that approach to life that’s made her a success, and it’s an approach that we’d all be well advised to adopt in the face of personal and societal adversity.

Wisdom about money, investing and life can be found anywhere. If you have a good quote that you’d like me to share with your fellow readers, send it to me, along with any comments, questions and suggestions you have about my newsletters, seminars or anything else. Click here to ask Jim.

Jim Woods is a 30-plus-year veteran of the markets with varied experience as a broker, hedge fund trader, financial writer, author and newsletter editor.

His books include co-authoring, “Billion Dollar Green: Profit from the Eco Revolution,” and “The Wealth Shield: How to Invest and Protect Your Money from Another Stock Market Crash, Financial Crisis or Global Economic Collapse.” He’s also ghostwritten many books and articles, as well as edited content for some of the investment industry’s biggest luminaries. Read more about Jim Woods.