Evergrande and the False Equivalence Fallacy

The big buzz in markets over the past several days, and particularly during Monday’s approximately 2% tumble nearly across the board, has been over what many are calling a potential “China Lehman Moment.”

Those of us in the markets in 2008 remember quite well the real “Lehman Moment,” because that is when the financial giant declared bankruptcy due chiefly to massive mortgage-based derivates defaults. That bankruptcy ushered in the financial crisis and the subsequent tanking of financial markets worldwide, along with the global economy.

Well, in China, that nation’s second-largest property developer, Evergrande, is thought to be ready to default on its massive debt payments. In fact, Evergrande already alerted banks that it would be unable to meet existing debt obligations, and last week, that prompted a huge drop in the Chinese real estate sector.

Over the weekend, investors around the world considered the potential contagion from the Evergrande situation (along with a handful of other unknowns such as Fed policy, tax hikes, the debt ceiling debate and earnings warnings), and on Monday morning, the markets went into serious risk-off mode.

Now, over the past week or so I have read many articles about Evergrande that basically argued that if the company defaults on its debt, that will pose a systemic risk to the Chinese economy, and that it could potentially be China’s very own Lehman moment. Because of this risk, and due to China’s significance to the global economy, investors took the cautious route on Monday and de-risked nearly across the board.

And while that de-risking is certainly understandable, I think equating Evergrande with Lehman Brothers is an example of what philosophers call the “false equivalence fallacy.”

The false equivalence fallacy occurs when a uniformity is drawn between two subjects based on flawed or false reasoning. This fallacy also is known as a fallacy of inconsistency. Another more common way of elucidating the fallacy of false equivalence is via the cliché “comparing apples and oranges.”

Here, Lehman can be considered an apple, and Evergrande can be considered an orange. I say that because there is a huge difference between the government of the United States in 2008 and the government of China in 2021.

I think one of the best ways to think about China is that it’s a country, but it operates like a company. Yes, there are ostensibly “private banks” in China. And yes, there are “private corporations.” Yet, in the end, the Communist Party owns anything and everything, if it so chooses. Indeed, that government risk is one of the inherent dangers when investing in China.

Because of the Chinese government’s heavy hand in the nation’s industry, they also are very likely to backstop Evergrande and restructure that entity’s debt and/or just pay out the debt. You see, it’s because of this governmental backstop that Evergrande and Lehman are a case of false equivalence.

Unlike Lehman, there really isn’t global contagion risk with Evergrande because in the end, the loans to Evergrande were made by Chinese banks that are implicitly backstopped by the Chinese government, and the Chinese government’s balance sheet can easily handle the Evergrande losses, which are valued around $303 billion of liabilities.

Of course, I don’t mean to be dismissive here, as $303 billion of liabilities is catastrophic for most banks. But again, these banks aren’t truly private — at least, not like they are in the U.S. or in Europe. And while Western governments are hesitant to provide taxpayer support to bail out banks (we didn’t in the case of Lehman), in China it’s simply something that will be done to support the property market.

The fact is that the only way this would be a global systemic problem is if Western banks were on the hook for Evergrande’s debts (which they’re not). Moreover, the fact that Western banks were actually on the hook for defaulted Asian debt in the late 1990s is what prompted the appropriately named “Asian debt crisis.” That was a case of foreign money, leveraged hedge funds and banks that stood to lose big, and not a case of the Chinese government taking a loss.

So, despite concerns over the Evergrande debt issues, that matter remains largely an internal Chinese problem, and one that the Chinese government is likely to ameliorate.

Therefore, when it comes to Evergrande and Lehman, I want you to be a good philosopher and avoid the false equivalence fallacy. Or, more colloquially, don’t mix up your apples and oranges. One is for making pies, the other is for making screwdrivers.

***************************************************************

ETF Talk: Tapping into the Best-Known Equal-Weight ETF

This article is the first in a series exploring equal-weight ETFs.

After the market downturn last week, in which the S&P 500 fell 1.7% and the Dow lost 600 points, some investors are turning to equal-weight exchange-traded funds (ETFs) to cushion their portfolios against another downturn.

When an ETF’s portfolio is equally weighted, all companies or sectors in it are equally favored, regardless of market capitalization or size. This contrasts with a market-cap-weighted ETF, in which a specific sector or company can attain a disproportionate weight in the portfolio.

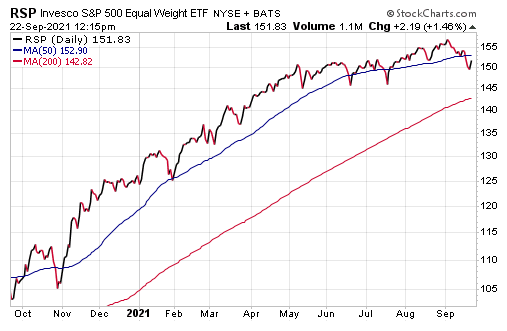

Thus, when setting a market-cap-weighted ETF and an equal-weight ETF with the same stocks in each portfolio side-by-side, we can see that those funds fill their holdings differently. One of the most famous equal-weight ETFs is one that my Successful Investing and Intelligence Report readers will find familiar, as it has been a mainstay in our Growth and Tactical Trends Portfolios since November 2020: the Invesco S&P 500 Equal Weight ETF (NYSEARCA: RSP).

Not surprisingly given the ETF’s name, RSP takes all the stocks in the S&P 500 and weights them equally. As a result, many small-cap and mid-cap stocks that would be overshadowed in a market-cap-weighted portfolio get their chance to shine more brightly in an equal-weighted ETF. At the same time, since the portfolio does not favor a specific sector, the ETF is relatively well-cushioned from sector downturns.

Some of the fund’s holdings include Centene Corporation (NYSE: CNC), American Airlines Group, Inc. (NASDAQ: AAL), Incyte Corporation (NASDAQ: INCY), EOG Resources, Inc. (NYSE: EOG), Lumen Technologies, Inc. (NYSE: LUMN), Cabot Oil & Gas Corporation (NYSE: COG), Expedia Group, Inc. (NASDAQ: EXPE) and Diamondback Energy, Inc. (NASDAQ: FANG).

This fund’s performance has been relatively strong, even when including the damage done by the COVID-19 pandemic. As of Sept. 21, RSP has been down 2.07% over the past month and up 0.77% for the past three months. It currently is up 18.64% year to date.

Chart courtesy of www.stockcharts.com

The fund has amassed $29.19 billion in assets under management and has an expense ratio of 0.20%. While RSP does provide an investor with a way to profit from an equally balanced portfolio, this kind of ETF may not be appropriate for all portfolios. Thus, interested investors always should conduct their due diligence and decide whether the fund is suitable for their investing goals.

As always, I am happy to answer any of your questions about ETFs, so do not hesitate to send me an email. You just may see your question answered in a future ETF Talk.

*****************************************************************

In case you missed it…

The New Volatility Explained

All of a sudden, the market is volatile… but why?

That was one of the main topics of conversation I had with investors over the past couple of days at the Las Vegas MoneyShow. In fact, I fielded a lot of questions about why stocks wobbled last week, and that’s completely understandable.

Fortunately, I was well-equipped to answer these questions. You see, when it comes to understanding the underlying reasons why markets behave as they do, you have to think a bit deeper than just the headlines.

Indeed, that’s why I call this publication “The Deep Woods,” because it is here that we peel back the surface layers of the onion skin so that we can get deep into the real reasons why things are as they are. In doing so, we can get a much greater sense of where things might likely go in the future. That’s because when you have a good sense of why things are the way they are, you have an even better chance of being right about how things are going to be in the future. And when it comes to our money, knowing what is likely to happen going forward is essential to investing success.

Your editor at the Eagle Financial Publications booth, Las Vegas MoneyShow.

So, why did market volatility pick up last week? Well, first there were lingering concerns about the health of the economic recovery after the soft August jobs report and the increasing threat of a more “hawkish” shift at global central banks. Then there was a soft German ZEW Survey, which offset bullish Chinese export data. Politically, there was a Wall Street Journal article that warned corporate tax rates could rise before the end of the year, and that further pressured stocks.

Another reason for last week’s volatility and subsequent selling was that the Treasury Department said the federal government would hit the debt ceiling in October, which was sooner than previously thought. The market will soon have to deal with what is potentially another volatility-inspiring political battle over raising the debt ceiling.

And while I suspect the outcome here will be as it always is, i.e., yet another raising of the debt ceiling, there will be more volatility in markets as the battle on this issue in Washington rages. Finally, last week, stocks bounced around as derivatives trading continued to influence markets ahead of this week’s options and futures “quadruple witching” expiration.

So, last week we had 1) Confirmation of Fed and global central bank tapering, 2) Tax hike headlines, 3) Debt ceiling warnings and 4) A series of earnings warnings related to the COVID-19 spike and subsequent margin pressures.

Yet while all of these are legitimate headwinds, the first three issues we’ve known about for some time — it’s just now the market has to deal with them as they are all coming to a head (tapering, tax hike headline risk and debt ceiling drama). However, none of these got materially worse last week, it’s just investors can’t ignore them anymore as a future risk. But while these events will continue to cause volatility, they are unlikely to be bearish gamechangers unless there’s a major surprise (accelerated tapering, massive tax hikes or a debt ceiling breach).

The one headwind here that I am most concerned about is fundamental, and it is one that we have been watching closely and writing about every day in the “Eagle Eye Opener,” our daily “insider” market briefing designed to give you this type of market analysis in your inbox every morning at 8 a.m. Eastern.

That headwind is earnings, and last week, we saw numerous businesses from multiple industries (industrials, airlines, grocery stores) issue earnings warnings on a combination of reduced demand (airlines), supply chain issues (industrials) and margin compression (grocery stores). If expected earnings growth begins to suffer at the hands of inflation, supply chain issues or margin compression, then that is something more substantial we need to consider.

The following is an excerpt from the “Eagle Eye Opener” dated Sept. 13, and it explains in detail why earnings growth is so important to understanding what could happen in markets next.

The market is trading at 20X expected 2022 S&P 500 EPS of $220. That’s 4,400 in the S&P 500. But if expected 2022 EPS falls to $210, then the general market “ceiling” would be 20 * 210, or 4,200. That’s more than 5% lower from here. Worse still, it’s unlikely the market would trade at a 20X multiple if earnings expectations were falling, which would put a “reasonable” level of the S&P 500 even lower (around 4,000, more than 10% lower).

Positively, a few earnings warnings don’t mean we’re going to see the overall EPS target for the S&P 500 materially cut. But this is a risk we need to watch closely, and you can be assured we will do just that.

In sum, the declines in stocks last week weren’t because the outlook turned materially worse, it did not. However, at these levels and these valuations the S&P 500 has essentially zero room for error. And as investors are forced to digest tapering headlines, tax hike threats, debt ceiling earnings and other issues, we should expect more volatility and the chance of a quick 5%-10% “air pocket” remains very real.

The bottom line here is that we all should expect to see more volatility in the coming weeks; however, more volatility doesn’t mean the end of the broader market rally.

And with the help of this publication, and with the daily analysis subscribers get in the “Eagle Eye Opener,” we can help you focus on making sure you can quickly differentiate between market “noise” and real, legitimate bearish gamechangers as we move towards Q4 and into the year’s end — and what can be better than that?

*****************************************************************

The Wisdom of Mistakes

“More people would learn from their mistakes if they weren’t so busy denying them.”

— Harold J. Smith

Learning from our mistakes is critical to our growth. Unfortunately, far too many people fail to even acknowledge their mistakes when it is painfully obvious to all that a mistake has occurred. Politicians are particularly guilty of this, so is it any wonder why so many policies out of Washington end up being repeated and harmful mistakes? If you want to be a better human, start by acknowledging your mistakes. Then, have the wisdom to learn from them, and make a valiant attempt not to repeat them. Doing so will put you on the path to excellence, and I guarantee you it will prompt a renewed sense of admiration in you from your friends, family and colleagues.

Wisdom about money, investing and life can be found anywhere. If you have a good quote that you’d like me to share with your fellow readers, send it to me, along with any comments, questions and suggestions you have about my newsletters, seminars or anything else. Click here to ask Jim.

Jim Woods is a 30-plus-year veteran of the markets with varied experience as a broker, hedge fund trader, financial writer, author and newsletter editor.

His books include co-authoring, “Billion Dollar Green: Profit from the Eco Revolution,” and “The Wealth Shield: How to Invest and Protect Your Money from Another Stock Market Crash, Financial Crisis or Global Economic Collapse.” He’s also ghostwritten many books and articles, as well as edited content for some of the investment industry’s biggest luminaries. Read more about Jim Woods.