Five Minutes with Dave Rubin

I’ve always been drawn to controversial figures.

I think the reason why is because even if I disagree with their ideas, I usually admire their willingness to come out and take a resolute stand in defense of their values.

Unfortunately, in the era of social media dominance and progressive cancel culture, standing up for one’s values — especially if they are deemed controversial in any way — brings with it a whole lot of negative consequences. Fortunately, that controversy also can translate into a clear-thinking voice that demands to be heard.

One such voice is Dave Rubin.

During the recent FreedomFest conference in Rapid City, South Dakota, I spoke with the talk show host and creator of “The Rubin Report,” ideas activist and author, as he came by for a quick visit to the set of the Way of the Renaissance Man podcast.

Although brief, our discussion covered several interesting topics, including Dave’s journey from progressive to classical liberal, the rising power of “Big Tech,” and the problems it’s brought to the issues surrounding free speech. We also talked about Dave’s entrepreneurial solution to this problem, a solution that’s based on competition and providing consumer alternatives to existing social media platforms.

One thing that I find extremely refreshing about Dave Rubin is his willingness to change his position on issues based on the integration of new facts and based on a questioning of the very premises he once lived by.

For many of us, including myself, it’s hard to step out of our current mindset and try to see the world differently. Yet I think doing so is important for self-knowledge. It’s also important in terms of cultivating a reality-based mindset free of the baggage of what we are taught we are supposed to think.

Rubin does a fantastic job of explaining his evolution from progressive to classical liberal in his February 2017 video “Why I Left the Left,” which can be found at PragerU, the education website of my Salem Media colleague and radio talk show host Dennis Prager.

As Rubin explained, “Over the last couple years, the meaning of the word ‘progressive’ has changed. Progressives used to say, ‘I may disagree with what you say, but I will fight to the death for your right to say it.’ Not anymore. Banning speakers whose opinions you don’t agree with from college campuses — that’s not progressive. Prohibiting any words not approved of as ‘politically correct’ — that’s not progressive. Putting ‘Trigger Warnings’ on books, movies, music, anything that might offend people — that’s not progressive either.”

Rubin goes on to say, “All of this has led me to be believe that much of the Left is no longer progressive, but regressive. This regressive ideology doesn’t judge people as individuals, but as a collective.”

Here is an example of why I admire Dave Rubin, as he was willing to take a look at reality for what it had become, and he was able to alter his views and his positions, and at some considerable cost to his comfortable status as a host of the popular show “The Young Turks,” based on his own rational judgement.

I think that if more of us had that kind of questioning spirit and the willingness to alter our ideas in the face of strong evidence, and/or the absence of evidence, the world would be a much different, and dare I say, a much more rational place.

If you would like to see my discussion with Dave Rubin, which includes more of my thoughts on him and the role he’s playing in the current debate on free speech and social issues, then I invite you to check out my latest podcast, “Five Minutes with Dave Rubin.”

***************************************************************

ETF Talk: U.S.-based Software Stocks Offered Through This ETF

COVID-19 created a demand for advances from technology and software companies that investors may want to use to pursue profits.

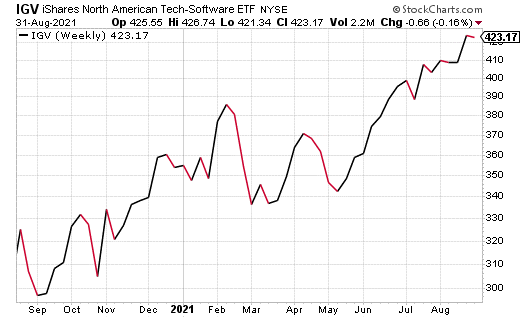

The Delta variant of COVID-19 may be spurring demand for services that require the latest software. So, perhaps it’s time to look at an exchange-traded fund (ETF) that offers broad exposure to large- and mid-cap technology and software stocks: iShares Expanded Tech-Software Sector ETF (BATS:IGV).

The ETF offers diverse exposure to the North American software industry and focuses solely on U.S.-based companies. The fund caps individual security weights at 8.5%, which allows for broader coverage in a concentrated industry.

IGV invests primarily in mid-cap software firms, allowing investors access to a decent amount of lesser-known, potentially high-growth firms. However, though the ETF invests in primarily mid-caps, it holds an array of well-known firms, as well. The ETF’s management reviews the fund’s holdings semiannually in June and December, and the weight caps are applied quarterly, starting in March.

On December 24, 2018, IGV changed indexes, but the new index is functionally identical. The main difference is that the new one includes specific companies by name, including Activision Blizzard (NASDAQ: ATVI), Electronic Arts, Inc. (NASDAQ: EA) and Snap Inc. (NYSE: SNAP). The index change seems to be a savvy move, since these companies, and others, were reclassified into the new Communications Services Sector near the end of 2018. Those stocks would have been removed from the fund, but the index change allowed them to remain in the Technology and Software sector.

IGV has an expense ratio of 0.43% and a 0.02% distribution yield, with an upcoming ex-dividend date set for Sept. 24. The ETF has $5.63 billion in assets under management and $4.92 billion in net assets.

The fund, which was created in 2001, is currently going strong. In late 2020, the ETF saw a considerable dip but then spiked in mid-March 2021. After two smaller dips, it began recovering in mid-May. Since then, the fund has climbed steadily and is currently at the high end of its 52-week range that has reached as high as $426.74.

Altogether, this open-ended fund seems to be seeing solid upward movement and an increased level of buyer interest.

Chart courtesy of www.stockcharts.com

The ETF’s top five holdings include Adobe Inc. (NASDAQ:ADBE), 9.11%; Microsoft Corp. (NASDAQ:MSFT), 8.70%; Salesforce.com Inc. (NYSE:CRM), 8.25%; Oracle Corp. (NYSE:ORCL), 6.25%; and Intuit Inc. (NASDAQ:INTU), 5.72%.

Not only is IGV a good segue into the software industry, but its mid-cap and large-cap holdings provide diverse exposure to lesser-known companies. As it concentrates on North American stocks, it may hold extra appeal for those, like me, who consider themselves patriotic.

For investors looking for a sensible approach to software exposure, iShares Expanded Tech-Software Sector ETF (BATS:IGV) may be worth looking into. However, it is important that all investors conduct their own due diligence prior to investing.

As always, I am happy to answer any of your questions about ETFs, so do not hesitate to send me an email. You just may see your question answered in a future ETF Talk.

*****************************************************************

In case you missed it…

Fed Tapers Matter

Over the past few years, we’ve all come to know the phrase “Black Lives Matter.” And regardless of what you might think about the organization of the same name (I have distinctive thoughts, but that’s for another time), one thing that must be said is that they did come up with a positive branding hook with the name. In fact, the name is so catchy that others have modified it to say, “Blue Lives Matter” and “All Lives Matter.”

Now, I have my own spin on this phrase, and I apply it to various aspects of life. “Rational Lives Matter” is my main motto, as that reflects my reverence for reason as man’s primary tool of survival. Then there’s “Nine Lives Matter,” which expresses my love of felines, and particularly Persian cats. Yet because so much of my own life is dominated by the financial markets, I now have come up with a spin on the phrase, and that spin is “Fed Tapers Matter.”

You see, when it comes to the Federal Reserve and its current bond-buying program, also known as quantitative easing (QE), the consensus is that “tapering” of its bond purchases is going to begin very soon. Yet what really matters here is not when the Fed tapers, but how the Fed tapers. Stated differently, “Fed Tapers Matter.” Allow me to explain.

Today, I am going to share an excerpt from my daily morning intelligence briefing, the “Eagle Eye Opener.” This is from the Tuesday, Aug. 24, edition, and I wanted to share it with you because I think it shows you the level of insightful analysis you get each trading day.

Now, as much as I would like to take full credit for this analysis, I cannot. That’s because the “Eagle Eye Opener” is a joint venture between me and my “secret market insider,” a man who provides this same insight to thousands of high-profile market professionals each morning. So, we (if you’re a subscriber) get to benefit from the same morning intelligence briefing that the “big boys” do, and we get it in our Inbox at 8 a.m. EST each trading day

So, let’s dig right into the analysis of why “Fed Tapers Matter

***

The S&P 500 and Nasdaq both hit new all-time highs on Monday, and if there was a “reason” for the rally, it’s growing sense that the Fed won’t taper as aggressively as some had feared just a few weeks back.

This idea has been percolating with investors since midweek last week (it was also why stocks rallied on Friday) but the announcement Monday morning that the Jackson Hole Central Bank Conference would have increased COVID-19 mitigation procedures and that Federal Reserve Chairman Jerome Powell would give his speech virtually drove home the point that the Fed has noted the spike in COVID-19 cases and the Delta-inspired headwind on the economy (albeit a mild headwind for now).

Those changes prompted the market to begin to anticipate a “dovish” Powell at Friday’s Jackson Hole speech, so given this influence we want to lay out a “Good, Bad and Ugly” scenario analysis for tapering, so we know what the market will likely do depending on Powell’s speech. Now to be clear, we don’t expect Powell to give any specifics on tapering Friday, but he should clearly “warn” the market that it’s coming. The key will be whether he stresses how gradual tapering will be.

“The Good Taper.” The Fed begins tapering in December and at $5 billion or $10 billion/month, essentially leaving QE ongoing for most (or all) of 2022. Likely Market Reaction: Risk on. The market is still viewing the Delta variant and COVID-19 spike as a temporary influence, so if the Fed tapered more slowly in response to it that would create an environment where the economic recovery resumes as COVID-19 peaks, but it’d still have the tailwind of QE for basically all of 2022. I’d expect stocks to rally (the S&P 500 could push towards 4,750 or higher as multiples could expand) led by cyclicals and growth/commodities. Treasury yields would rise but not materially given the Fed will continue to buy Treasuries throughout 2022. But I’d still expect the 10-year yield to hit 2% in the coming quarters. The dollar would drop sharply (likely through 92) while commodities would be the biggest winners from this decision (oil and gold should surge on the weaker dollar and higher sustainable inflation).

The “Bad Taper.” The Fed does as expected and begins tapering in December at a rate of $15 billion/month, ending QE in mid 2022. This outcome isn’t really “bad” because it’s already mostly priced into markets, but with COVID-19 cases high again and some rising concerns about growth, the market would be more sensitive to the Fed following this procedure. But as long as the market views the COVID-19 spike as temporary (and it still very much does) then this tapering schedule won’t derail the rally. Likely Market Reaction: Not much. Stocks could drop modestly on a knee-jerk “tapering is bad” tantrum, but again, this has been widely telegraphed so I wouldn’t expect too big of a move. Defensives and super-cap tech would outperform cyclicals and value. Treasury yields should rise back into the upper 1.50% range on this outcome in the coming months, although again I don’t think the increase in the 10-year yield would be “disorderly.” The dollar shouldn’t move much, as at 93 this outcome is already priced in, and the same can likely be said for commodities (again they are off recent highs, and this is largely priced in).

The “Ugly Taper.” The Fed begins tapering QE in December at a rate of $30 billion/month (or more than $15 billion), ending QE before June 2022. This would be a shock to markets and substantially increase stagflation concerns, because the Fed aggressively tapering QE with the uptick in COVID-19 cases would clearly signal that the Fed is nervous about inflation regardless of the loss of growth. Likely Market Reaction: Pain. Stocks would drop sharply led by cyclical sectors such as energy, materials, and consumer discretionary. Super-cap tech, consumer staples and some financials (benefitting from higher rates) would relatively outperform but the entire market would be sharply lower. Treasuries would drop/yields would surge (10-year yield likely towards 2%), as would the dollar (the Dollar Index would rise towards 95). Commodities would be the biggest loser in this scenario and gold would get hit very, very hard.

Would a “No Taper” be good for stocks? No (at least not beyond the very short term). Markets might be inclined to think a total delay of tapering would be good for stocks, but that’s not likely the case beyond an initial (dovish is good) pop in markets. I say that because sustainably high inflation is much, much bigger medium- and long-term risk to stocks than COVID-19 (as long as the vaccines hold the line), because too-high inflation will ultimately result in the Fed hiking rates more quickly and crushing the economy (see 1970/early 1980). In the meantime, assets could rise but corporate margins would continue to get squeezed. Bottom line, a tapering delay would spark a short-term rally, but we’d be looking to get majorly defensive after that initial pop. Keeping inflation under control is much more important for the long-term health of the bull market than anything else.

How the Fed tapers is the next major variable for this market (again assuming the COVID-19 cases do subside like they have in India and the UK) and how the Fed tapers will dictate whether that’s a tailwind or a headwind for stocks. Again, we do not expect these specifics to be announced on Friday. They will come at the September meeting. But we do expect Powell to hint at an outcome and given the Fed’s changes to the conference (masks, more social distancing, Powell virtual), if there’s going to be a surprise it’s likely dovish.

***

Well, there you have it. This is the kind of masterful, high-level market analysis you will find each and every morning when you subscribe to the “Eagle Eye Opener.” So, if you want the kind of market intelligence that the pros get every morning, and at a cost of about one nice dinner every quarter, then I invite you to check out the “Eagle Eye Opener” right now — it might just be the best decision you’ve made all summer.

*****************************************************************

Bueller? Bueller?

“The question isn’t ‘What are we going to do?’, the question is ‘What aren’t we going to do?’”

— “Ferris Bueller’s Day Off”

The 1980’s classic about a rebellious and wily teen who lives life to the fullest is one of the best films ever made when it comes to showing the virtue of being a free spirit. If you haven’t watched this film in a while, I recommend doing so. It might just awaken that irreverent inner teen in you, and it will definitely make you smile.

Wisdom about money, investing and life can be found anywhere. If you have a good quote that you’d like me to share with your fellow readers, send it to me, along with any comments, questions and suggestions you have about my newsletters, seminars or anything else. Click here to ask Jim.

Jim Woods is a 30-plus-year veteran of the markets with varied experience as a broker, hedge fund trader, financial writer, author and newsletter editor.

His books include co-authoring, “Billion Dollar Green: Profit from the Eco Revolution,” and “The Wealth Shield: How to Invest and Protect Your Money from Another Stock Market Crash, Financial Crisis or Global Economic Collapse.” He’s also ghostwritten many books and articles, as well as edited content for some of the investment industry’s biggest luminaries. Read more about Jim Woods.